FinSight AI

Short-term stock-movement classification fusing market indicators, financial-news sentiment, and document retrieval.

- Python

- PyTorch

- FinBERT

- Transformers

- RAG

- scikit-learn

- Metric shown

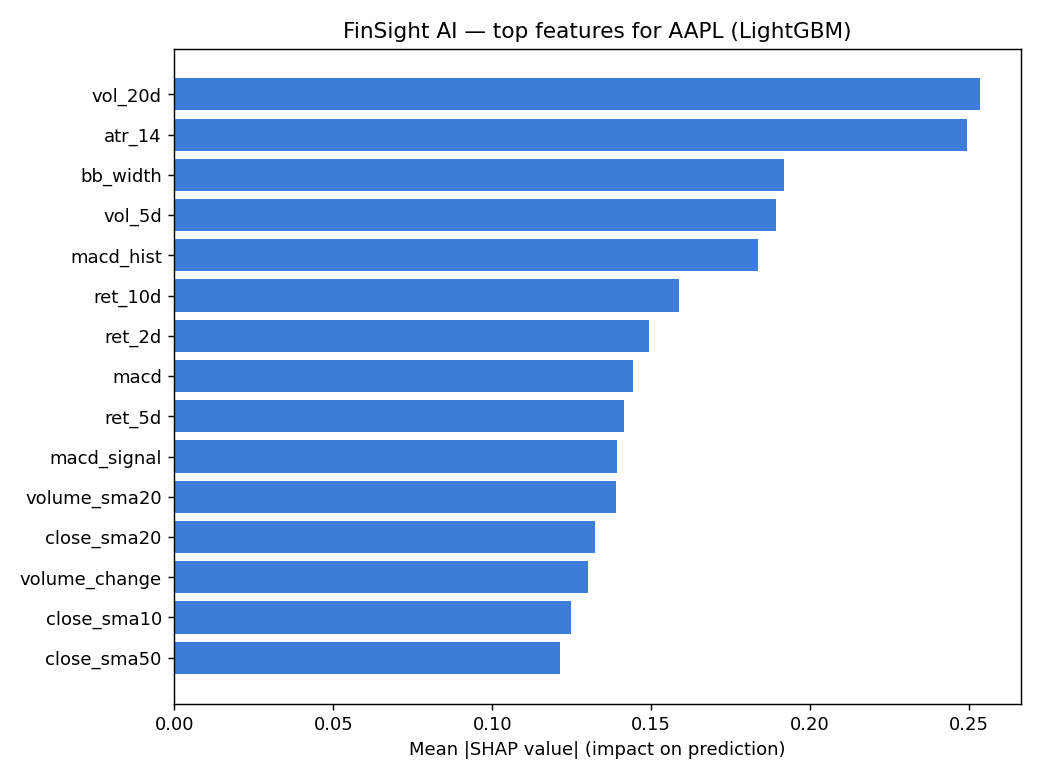

- SHAP explainability

- Reproducible pipeline

- Docker included

- CI/tests included

At a glance

- Problem

- Can short-term stock direction be predicted using market data, news sentiment and retrieved document context?

- Built

- End-to-end financial ML pipeline with technical indicators, FinBERT sentiment and document retrieval.

- Models / methods

- Logistic regression, random forest, gradient boosting, LSTM, GRU and Transformer-style models.

- Result

- Models performed only slightly above baseline, showing the difficulty of short-horizon prediction.

- Strength shown

- Leakage-free evaluation, reproducible experiments, honest reporting.

- Links

- DashboardCase StudyRepo available on request

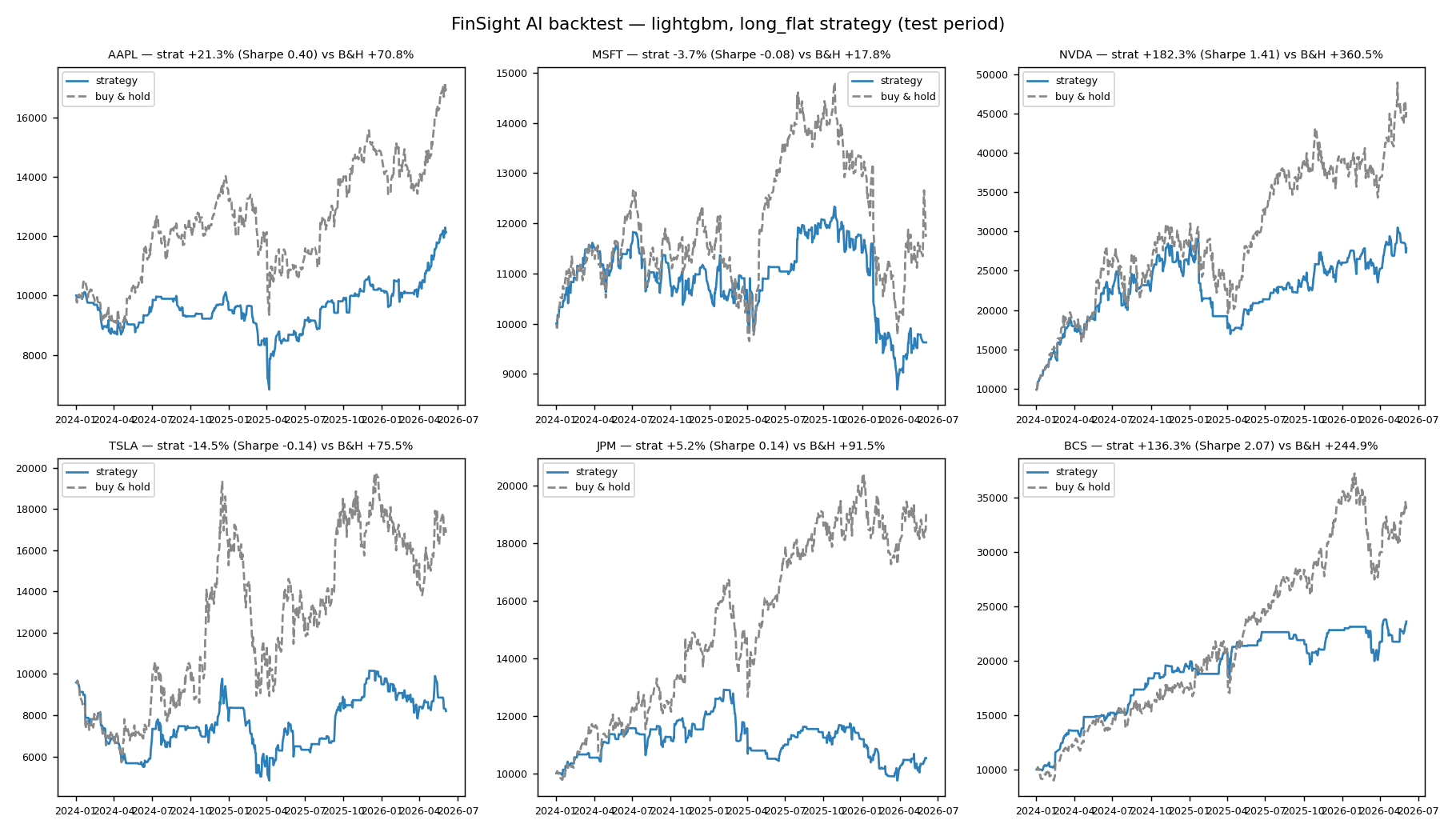

Visual proof

Charts and diagrams are real outputs and architecture from the project.

01Objective

Predict whether a stock moves UP, DOWN, or SIDEWAYS over the next few trading days, and test honestly whether news sentiment and document context improve on price-only models.

02Dataset / input

- Daily OHLCV price history for a basket of large-cap tickers

- Engineered technical indicators (returns, moving averages, RSI, MACD, volatility)

- Financial-news headlines scored for sentiment with FinBERT

- Filings and reports indexed for retrieval-augmented context

03Model approach

- Framed as a 3-class problem with strict, leakage-free time-based splits

- Classical baselines: logistic regression, random forest, gradient boosting

- Deep sequence models: LSTM, GRU and a Transformer-style encoder

- Ablations to isolate the contribution of sentiment and retrieval

04Results / metrics

Evaluated with macro-F1 to respect class imbalance. Models clustered just above the random baseline (0.33) — the honest finding that 5-day direction is close to unpredictable on this universe. SHAP confirmed the models leaned on volatility and momentum signals rather than artefacts.

05Deployment / reproducibility

Packaged as a modular pipeline with a single config, unit tests, a Streamlit dashboard, a Dockerfile, and CI — so every experiment is reproducible end to end.

06Limitations

- Short-horizon market direction is inherently noisy and near-random

- Sentiment used a reproducible sample feed rather than a paid dated archive

- Single market, daily resolution, a handful of tickers

07Future improvements

- Sector-specific market context and a real dated news API

- Walk-forward cross-validation and probability calibration

- A FastAPI inference service alongside the dashboard

08Key takeaway

A negative result, reported honestly: the engineering rigour (leakage-free splits, ablations, reproducibility) matters more than chasing an inflated score on a near-random problem.